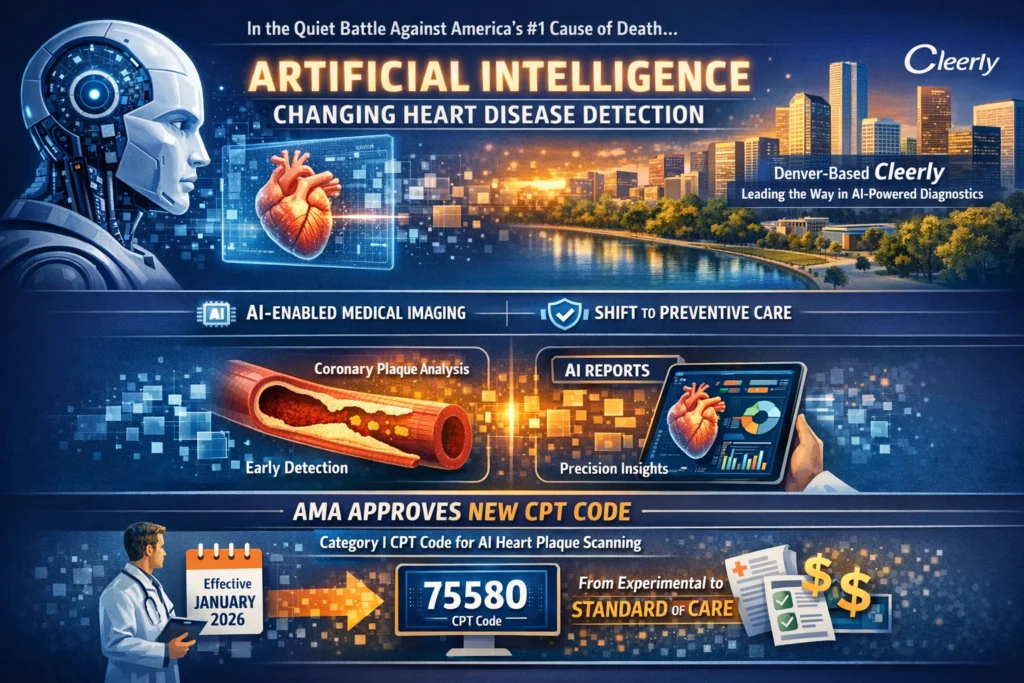

In the quiet battle against America’s leading cause of death, a new weapon has emerged—one that doesn’t wield a scalpel or prescribe a pill, but rather analyzes images with a precision beyond human capability. This weapon is artificial intelligence, and it’s revolutionizing how we detect and treat disease before symptoms even appear.

At the forefront of this transformation stands Cleerly, a Denver-based healthcare technology company that has positioned itself at the intersection of two powerful trends: the explosion of AI-enabled medical devices and a fundamental shift in how insurers pay for preventive care. When the American Medical Association (AMA) issued a new Category I CPT code for AI coronary plaque scanning—effective January 2026—it did more than create a billing checkbox. It signaled official recognition that artificial intelligence has matured from experimental novelty to evidence-based standard of care.

The Cleerly Story: Building a World Without Heart Attacks

Founded in 2017, Cleerly emerged with an audacious mission: “creating a world without heart attacks.” The company’s approach is elegantly simple in concept yet remarkably complex in execution: use artificial intelligence to analyze coronary computed tomography angiography (CCTA) images and quantify exactly what’s happening inside the arteries that supply blood to the heart.

Traditional approaches to heart disease assessment have relied heavily on indirect markers. A stress test might reveal that blood flow is restricted. A calcium score might suggest the presence of plaque. But these methods leave physicians and patients in the dark about the true nature of the disease. Is the plaque stable or vulnerable to rupture? Is it calcified or non-calcified? How much of the artery is affected?

Cleerly’s platform answers these questions with unprecedented specificity. Using proprietary machine learning algorithms that have received FDA clearance, the system non-invasively detects and quantifies atherosclerosis by measuring plaque volume, composition, length, and location. It evaluates stenosis severity and can even detect ischemia—reduced blood flow—providing a comprehensive picture of coronary artery disease that was previously only available through invasive procedures.

The company’s technology, marketed as Cleerly Labs, represents a fundamental shift in cardiovascular care. Rather than waiting for patients to develop symptoms—by which time the disease may have been progressing silently for decades—Cleerly enables clinicians to identify and characterize heart disease at its earliest stages. This proactive approach aligns perfectly with the broader healthcare industry’s move toward value-based care, where preventing expensive acute events like heart attacks becomes financially as well as clinically desirable.

Investors have taken notice in a big way. Cleerly has raised an astonishing $388.55 million across multiple funding rounds. In December 2024 alone, the company secured a $106 million Series C extension led by Insight Partners and Battery Ventures. Previous backers include Vensana Capital and New Leaf Venture Partners, a who’s who of healthcare and technology investors betting big on AI’s potential to transform medicine.

The Reimbursement Tipping Point: AMA’s New CPT Code Changes Everything

For all the technological wizardry behind Cleerly’s platform, the most significant development in its journey may be a bureaucratic one. The American Medical Association’s decision to issue a new Category I CPT code for AI coronary plaque scanning, effective January 2026, represents what industry insiders call a “reimbursement tipping point.”

To understand why this matters, consider the economics of medical innovation. Developing AI-powered diagnostic tools requires millions of dollars in research, clinical validation, and regulatory approval. Hospitals and imaging centers, in turn, must invest in new technology and training. Without clear pathways for reimbursement, adoption stalls. Why purchase expensive AI software if insurers won’t pay for the scans it analyzes?

The AMA’s Category I CPT code designation signals that the medical establishment recognizes AI plaque analysis as a proven, effective procedure with sufficient evidence to warrant standard payment. This is the highest level of coding recognition, reserved for procedures that are widely performed, have established clinical efficacy, and are supported by the medical community.

The practical implications are enormous. Starting in January 2026, when a physician orders an AI-powered plaque analysis, they can bill insurance using a dedicated code specifically for that service. This creates a reliable revenue stream that justifies the investment in AI technology. More importantly, it removes the financial uncertainty that has historically slowed adoption of innovative diagnostics.

Cleerly has already been laying the groundwork for this reimbursement revolution. In September 2025, the company announced that Cigna would begin covering its Cleerly LABS Advanced Plaque Analysis starting October 1, 2025. This made Cigna the latest major insurer to recognize the value of AI-powered cardiovascular imaging, following similar moves by other payers. The AMA’s coding decision effectively nationalizes and standardizes what was previously a patchwork of individual insurance decisions.

The economic impact extends beyond Cleerly itself. According to Fortune Business Insights, the global AI in medical imaging market was valued at $1.88 billion in 2025 and is projected to reach a staggering $299.5 billion by 2034, growing at a compound annual rate of 36.91%. Other analysts are even more bullish. Precedence Research estimates the market could hit $22.97 trillion by 2035, though this figure appears to include broader economic impacts rather than direct market size. Whatever the exact numbers, the trajectory is clear: AI in medical imaging is one of the fastest-growing sectors in healthcare.

Beyond the Heart: AI’s Expanding Role in Medical Imaging

While Cleerly focuses on cardiovascular applications, the AI diagnostics revolution extends across nearly every domain of medical imaging. The U.S. Food and Drug Administration has approved over 1,400 “AI-enabled” devices for medical use, with the vast majority related to radiology. According to analysis published in JACC: Advances, more than 1,000 AI-enabled products were reviewed by the FDA from 1995 through 2024, with 85% approved in just the last six years.

Radiology dominates this landscape for good reason. Pattern recognition through image analysis is one of AI’s fundamental strengths—it can identify subtle abnormalities in medical images more quickly and consistently than human observers. Over 700 FDA-authorized AI medical devices fall within radiology, followed by approximately 100 in cardiology and just over 30 in neurology.

The cardiovascular space, where Cleerly competes, has seen particularly rapid growth. JACC: Advances researchers identified 209 cardiovascular AI devices approved through 2024, with the most frequent applications including electrocardiography-based arrhythmia detection (21.1%), echocardiography (16.7%), and coronary artery disease detection and evaluation (16.7%). Cardiovascular imaging represents the largest subspecialty category at 25.4% of approved devices.

This proliferation of AI-enabled devices reflects both technological progress and regulatory pragmatism. Most devices—approximately 96%—receive clearance through the FDA’s 510(k) pathway, which requires demonstrating “substantial equivalence” to an already approved predicate device. This approach reduces the regulatory burden for incremental innovations while maintaining safety oversight. Only a handful of truly novel devices require the more rigorous premarket approval process.

The Evidence Base: Does AI Actually Improve Diagnosis?

The AMA wouldn’t have issued a Category I CPT code without compelling evidence, and the research supporting AI diagnostics is indeed impressive. A comprehensive meta-analysis published in July 2025 examined AI’s diagnostic effectiveness across multiple studies and found a combined area under the curve (AUC) of 0.9025—a measure of diagnostic accuracy where 1.0 represents perfection. This indicates that AI models demonstrate strong diagnostic capability across diverse applications.

The same analysis revealed important nuances. Subgroup analyses showed that convolutional neural networks—the type of deep learning architecture particularly suited to image analysis—achieved the highest accuracy. However, researchers also identified substantial heterogeneity across studies (I² = 91.01%), meaning that results varied considerably depending on the specific application, model architecture, and data quality. Domains like endocrinology showed greater performance variability, while image-heavy fields like radiology and cardiology demonstrated more consistent results.

Publication bias remains a concern. Studies with positive results are more likely to be published than those showing equivocal or negative findings, potentially inflating perceptions of AI’s capabilities. This underscores the importance of continued research, transparent reporting, and independent validation—precisely the kind of evidence generation that the AMA’s CPT code designation implicitly requires.

The JACC: Advances analysis raised additional concerns about demographic reporting. Only 10% of FDA approvals reported race or ethnicity data, more than three-quarters didn’t report the age of study participants, and a similar proportion omitted gender information. This lack of demographic transparency raises questions about whether AI algorithms perform equally well across diverse populations—a critical consideration as these tools are deployed in real-world clinical settings serving diverse patient communities.

The Regulatory Landscape: How AI Devices Reach Patients

Understanding how AI diagnostics reach clinical practice requires navigating the FDA’s regulatory framework for software as a medical device (SaMD). The FDA has been reviewing AI-enabled medical devices for three decades, with the first approval granted in 1995 to PAPNET, an automated system for analyzing cervical smears. However, the pace of approvals has accelerated dramatically in recent years.

Most AI-enabled devices follow the 510(k) pathway, which requires demonstrating substantial equivalence to an already approved device. This approach works well for incremental innovations but may stifle truly novel applications that lack predicates. As of October 2024, only 22 devices had received approval through the De Novo pathway for novel low-to-moderate risk devices without predicates, and just four required the most rigorous premarket approval process for high-risk devices.

The FDA has recognized that traditional medical device regulations weren’t designed for AI’s unique characteristics, particularly its ability to learn and evolve. In January 2025, the agency issued draft guidance on “Artificial Intelligence-Enabled Device Software Functions: Lifecycle management and marketing submissions recommendations,” proposing frameworks for managing AI throughout its lifecycle.

A key distinction in regulatory thinking involves “locked” versus “adaptive” or “continual” learning algorithms. Locked algorithms are fixed at the time of deployment and don’t change based on new data. Adaptive algorithms continue learning after deployment, potentially improving over time but raising questions about how to validate an algorithm that’s constantly evolving. The FDA is still working through these complexities, but the increasing number of approvals demonstrates that acceptable pathways exist.

Market Dynamics: Cloud, Costs, and Competition

The AI medical imaging market is being shaped by several powerful forces beyond just technological capability. Cloud adoption is accelerating access to AI imaging workflows, with hospitals moving imaging data and radiology IT systems to the cloud to overcome the limitations of slow, difficult-to-maintain on-premise systems. Cloud-based AI can be deployed and updated across multiple sites simultaneously, dramatically accelerating adoption.

However, significant barriers remain. Cybersecurity threats have emerged as a major concern, with incidents like the SimonMed Imaging data breach in March 2025 prompting tighter security reviews and extended sales cycles. Hospitals must balance the benefits of AI connectivity against the risks of exposing patient data and critical systems to cyberattacks.

Perhaps the biggest challenge, ironically, is reimbursement itself—or rather, the lack thereof for most applications. The AMA’s cardiovascular CPT code is the exception, not the rule. Most imaging AI tools operate within standard reading workflows—flagging abnormalities, detecting fractures, identifying nodules—making it difficult for payers to view them as separately billable services. Hospitals must often fund AI from operating budgets and justify the expense through internal ROI metrics like faster turnaround times, reduced repeat scans, and increased throughput.

The numbers tell a sobering story. In September 2025, Medicare denied approximately $16 million in radiology AI claims from the previous five years. A study in the Journal of the American College of Radiology found that of 83,392 AI service claims submitted between 2018 and 2023, nearly 53% were denied, representing $16.4 million in rejected payments. These denials slow adoption and make it harder for AI companies to demonstrate value to cost-conscious healthcare providers.

The Startup Ecosystem: Who’s Who in AI Diagnostics

Cleerly is far from alone in the AI diagnostics space. A vibrant ecosystem of startups is attacking medical imaging challenges from every angle, each with its own focus and approach.

Aidoc has built an AI-based enterprise platform called aiOS that analyzes medical images for critical findings like strokes and pulmonary embolisms, alerting care teams in real-time to speed diagnosis and treatment. The company focuses on integrating AI directly into clinical workflows, ensuring that time-sensitive conditions receive immediate attention.

Viz.ai takes a similar approach but emphasizes care coordination. Its platform detects conditions on scans and automatically notifies multidisciplinary teams, reducing diagnosis and treatment times for strokes and other time-sensitive conditions. The company has built a strong presence in neurovascular care while expanding into other areas.

Qure.ai focuses on global health applications, developing AI solutions for chest X-rays and head CT scans that assist in early detection of tuberculosis, lung cancer, and stroke. The company has particular traction in high-volume markets and emerging economies where radiologist shortages are most acute.

Subtle Medical takes a different tack, specializing in algorithms that enhance image quality and acquisition efficiency. Its technology allows for faster MRI and PET scans or lower radiation doses without compromising image quality—addressing the practical realities of imaging departments struggling with patient throughput.

CARPL.ai operates a radiology AI marketplace and enterprise imaging platform that helps hospitals access multiple AI tools through a single interface. The company recently added the World Bank Group’s International Finance Corporation as an investor, highlighting the global interest in AI diagnostics. CARPL.ai serves clients including Massachusetts General Hospital and works with the Government of India on tuberculosis screening programs.

Voio emerged from stealth in November 2025 with $8.6 million in seed funding to build what it calls “frontier AI for healthcare.” Founded by UC Berkeley and UCSF faculty, the company released Pillar-0, an open-source AI model that interprets medical images across hundreds of conditions with demonstrated accuracy improvements of 10-17% over leading models from Google, Microsoft, and Alibaba. The team’s previous breast cancer tool has been used in over 2 million mammograms worldwide, demonstrating real-world validation.

This diversity of approaches—from workflow integration to image enhancement to marketplace aggregation—reflects the maturity of the AI diagnostics field. No single company has all the answers, and the market is large enough to support multiple winners addressing different aspects of the imaging challenge.

Challenges on the Horizon

Despite the enthusiasm surrounding AI diagnostics, significant challenges remain before these technologies achieve their full potential.

Interoperability with legacy systems remains a persistent headache. Most hospitals operate on electronic health record and picture archiving systems that weren’t designed with AI integration in mind. Making AI tools work seamlessly within these environments requires custom integration work that slows adoption and increases costs.

Data bias and model generalizability raise fundamental questions about whether AI algorithms work equally well for everyone. If training data underrepresents certain populations, the resulting algorithms may perform poorly for those groups, exacerbating rather than reducing health disparities. The JACC: Advances analysis found that most FDA approvals lacked basic demographic reporting, making it impossible to assess whether approved devices have been validated across diverse populations.

Regulatory fragmentation across global markets complicates expansion for AI companies. While the FDA has developed workable pathways, European, Asian, and other regulators have their own requirements. Navigating this patchwork of regulations requires resources that many startups lack.

The need for explainable AI grows as these tools become more influential in clinical decision-making. Physicians are understandably reluctant to act on recommendations from systems that can’t explain their reasoning. The growing emphasis on explainable AI—systems that can articulate how they reached their conclusions—reflects this clinical reality.

The Future of Diagnostics

Looking ahead, several trends suggest how AI diagnostics will evolve.

Generative AI is moving into clinical practice, automating the creation of diagnostic reports and summarizing patient histories for radiologists. It’s also being used to create synthetic medical images that allow robust AI training without compromising patient privacy—a significant advance given the difficulty of obtaining large, diverse, real-world datasets.

AI-first workflows are becoming more common in forward-thinking healthcare systems. Rather than treating AI as an optional add-on, these workflows have algorithms pre-analyze scans to flag suspicious areas and prioritize urgent cases. This approach directly addresses radiologist shortages by handling routine tasks and allowing specialists to focus on complex cases.

Edge and embedded AI running on devices rather than in the cloud is gaining momentum, with some analysts projecting 30.80% CAGR for this segment. Edge AI reduces latency—critical in emergency settings—and addresses privacy concerns by keeping data local.

Digital twins—virtual models that replicate patients’ physiological characteristics by integrating diverse data sources—represent the next frontier. These models could enable continuous monitoring, early disease detection, and personalized treatment optimization in ways that episodic care never can.

Personalized medicine stands to benefit enormously from AI diagnostics. By integrating genetic, lifestyle, and health data, AI systems can generate tailored diagnostic strategies and treatment predictions that move beyond population averages. The combination of AI with genomics and continuous monitoring from wearables promises to make healthcare truly personalized for the first time.

Conclusion

The AMA’s decision to create a dedicated CPT code for AI coronary plaque scanning, effective January 2026, marks a watershed moment for AI diagnostics. It signals that artificial intelligence has crossed the chasm from experimental technology to standard of care—at least in cardiovascular imaging.

For Cleerly, the company at the heart of this story, the timing couldn’t be better. With nearly $400 million in funding, FDA clearance for its core technology, major insurers like Cigna on board, and now a dedicated reimbursement code, the company is positioned to capitalize on the growing recognition that preventing heart attacks requires seeing inside arteries before symptoms appear.

But the implications extend far beyond a single company or even a single disease. The AI diagnostics revolution is reshaping medicine from the ground up, starting with radiology and cardiology—the specialties most dependent on image interpretation—and spreading to every corner of healthcare. With over 1,400 FDA-approved AI-enabled devices and counting, the question is no longer whether AI will transform diagnosis, but how quickly and how completely.

The challenges ahead are real: reimbursement hurdles, interoperability headaches, validation gaps, and the persistent need for explainability and transparency. But the trajectory is clear. As the meta-analysis published in July 2025 concluded, AI demonstrates strong potential to enhance diagnostic accuracy and enable more personalized care. The evidence base is growing, the regulatory pathways are maturing, and the market is responding.

When the first AI-enabled medical device was approved in 1995, few could have predicted that three decades later, algorithms would be reading mammograms, quantifying coronary plaque, and detecting strokes before human eyes spot them. And yet here we are, on the cusp of 2026, with a CPT code that says, in the bureaucratic language of medicine, that this technology has arrived.

The algorithm will see you now. And it might just save your life.